I first came across the R&D tax credit not through a pitch or a mailer, but by sitting in on financial reviews at a DSO on the West Coast. I was not an accountant. I was there on the clinical side. But the practice had an open culture around sharing how the business worked, and I paid attention.

The DSO had engaged a specialty tax consulting firm to evaluate whether their activities qualified under Section 41 of the Internal Revenue Code. That is the statute that governs the Research and Development tax credit. The credit has been around since 1981 but a lot of smaller practices only started hearing about it in the last ten years or so, as firms began targeting healthcare and dental specifically.

The way the firm approached it was methodical. The IRS requires what is commonly called the four-part test. First, the activity has to be technological in nature, meaning it has to rely on hard science, engineering, or a similar discipline. Second, there has to be a permitted purpose, which in a clinical setting usually means improving a product, process, or technique. Third, there has to be what the IRS calls elimination of uncertainty, meaning you didn’t already know the outcome when you started. Fourth, and this is the one most firms focus on when pitching dentists, there has to be a process of experimentation, meaning you tried different approaches, tested, evaluated, and adjusted.

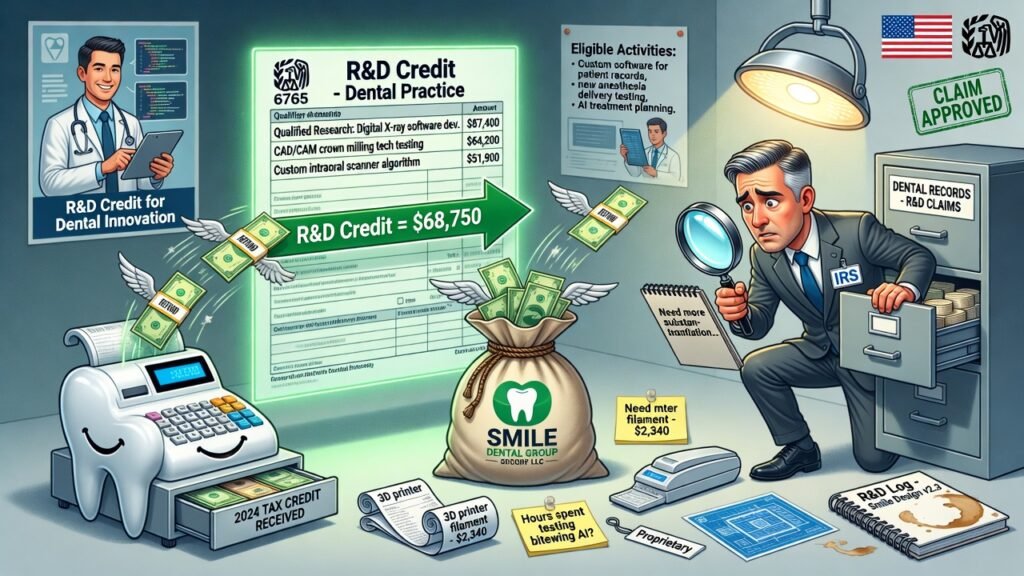

At the DSO, the firm spent several weeks interviewing clinical directors, going through treatment records, protocol documentation, and internal training materials. They were building what is called a contemporaneous record, which is essentially your evidence file if the IRS ever comes back and asks you to prove the claim. The credit they identified was based on qualified research expenses, which included a percentage of wages paid to staff engaged in qualifying activities and a portion of supply costs tied to those activities. For a group with multiple locations and a meaningful clinical development program, the numbers were real. We are talking about credits that are high six figures across multiple tax years over a cluster of sites.

The firm took a contingency fee, typically somewhere between 20 and 30 percent of the credit value. That is standard in this space. The DSO’s CFO was comfortable with it because the underlying documentation was solid and the firm had done this many times before.

When I got to Georgia for residency, I saw the other side. The school was doing genuine research. Residents were testing bracket systems, evaluating bone response to different expansion techniques, running clinical studies with IRB oversight. That work absolutely fits the framework. But in an academic setting, the funding and the tax treatment work differently. The institution files differently than a private practice would. What I took away from that environment was more about the substance of what actually qualifies, not the mechanics of filing.

Fast forward to when I started looking at this for my own practice. I have one location. My qualified research expenses, even if I applied a generous interpretation, would be a fraction of what a multi-location group produces. The credit under Section 41 is calculated using what is called the regular research credit method, which is 20 percent of qualified expenses above a base amount, or the alternative simplified credit, which is 14 percent of qualified expenses above 50 percent of your average qualified expenses from the prior three years. For a single orthodontic practice, if you are being honest about what truly qualifies versus what a firm would argue qualifies, you are maybe looking at a credit of $10,000 to $30,000 in a good year. That assumes you have real documentation and a defensible methodology.

Here is where the math stopped working for me. The IRS added the R&D credit to its list of transactions requiring heightened scrutiny. Small practices claiming credits disproportionate to their revenue size get flagged. The documentation requirement is not casual. You need to show time allocation by employee, tie specific activities to specific research questions, and be able to produce all of it on demand. For a small practice, building and maintaining that infrastructure costs real money and staff time.

I also looked at what the IRS has actually done in audits. There have been cases where small practices paid contingency fees to specialty firms, filed amended returns going back three years, and then received IRS examination notices. When the agent asked for the contemporaneous records, the documentation was thin. The credits got disallowed, the practice owed back taxes plus interest plus a 20 percent accuracy-related penalty in some cases. The firm that filed was long gone.

For me the decision was straightforward. A potential $15,000 to $20,000 credit, minus a 25 percent contingency fee, leaves you with maybe $12,000 to $15,000. Against that you are carrying audit risk, documentation overhead, and the practical reality that my practice is young and does not yet have three years of stable qualified expense history to anchor the base period calculation cleanly. The risk-reward did not make sense at this stage.

I am not saying the credit is illegitimate. When it is done right, with real documentation and a credible methodology, it is a legal and valid credit. What I am saying is that the way it gets sold to small and mid-size dental practices often glosses over the documentation burden and the audit exposure. The firms pitching it are not the ones sitting across from an IRS agent two years later. The practice owner is.

For another practice at a different scale, with a genuine clinical development program and the infrastructure to document it properly, the math might look completely different. That is a conversation worth having with a CPA who does not have a contingency stake in the outcome.